What does umbrella insurance cover?

Although the definition of coverage that is provided under an umbrella policy, at first glance, seems somewhat nebulous, it can be boiled down to 3 broad categories:

- Bodily injury liability covers the cost of injuries to another person, and may include the cost of medical bills and liability claims that are the result of injuries to:

- Other people, due to a car accident where the policyholder is at fault

- Other people, by a pet owned by the policyholder

- Guests in the policyholder's home, due to a fall or some other accident

- Property damage liability covers the cost of damage or loss to another person's tangible property, and may include the costs associated with:

- Damage to vehicles and other property, resulting from a car accident for which the policyholder is found at fault

- Claims incurred in connection with damage caused to the property of others

- Accidental damage caused to school property by a child

- Other personal liability covers other actions a policyholder could be sued for, such as:

- Slander (an injurious spoken statement)

- Libel (an injurious written statement)

- False arrest, detention, or imprisonment

- Malicious prosecution

- Mental anguish or shock

Weighing the costs and potential benefits

The price of obtaining $1 million of personal liability coverage from an umbrella policy is relatively low, generally costing between $150 and $300 per year, according to the Insurance Information Institute.1 And for every additional $1 million of financial protection, the incremental premium cost tends to gradually diminish.

From the insurer's perspective, the lower premium payments charged to purchase umbrella liability coverage reflect the fact that no payments are made until after the coverage limits of all other applicable policies have been exhausted. Bottom line: The probability of any claims being filed against an umbrella policy is relatively small, which results in a lower premium for the consumer.

Tip: Keep in mind that the cost of obtaining umbrella liability insurance can often be reduced even further: In most states, discounts are available if more than one policy is purchased from the same firm. This can make umbrella insurance less expensive if it is purchased from the same insurance company that covers your car, home, or boat.

Umbrella insurance providers will expect an applicant to have in place previously purchased auto, homeowners, or renters insurance before issuing such a policy. Most insurers will require an applicant to have a minimum of $250,000 of liability insurance on an auto insurance policy and about $300,000 of liability on a homeowners insurance policy before selling a $1 million umbrella insurance.

A potential pitfall in the world of insurance is a gap in coverage that can arise due to different expiration dates between your regular coverage (auto, home) and your umbrella policy coverage. The next time you change insurance agents, be aware that it is possible that coverage limits could be changed, say from $250,000 to $500,000 on an auto policy, potentially causing a gap in coverage with your umbrella policy.

Tip: One way to reduce the risk of any possible gap in coverage would be to have one insurance agency underwrite your underlying auto, homeowners and umbrella policies together, giving them the same expiration dates.

Related Articles

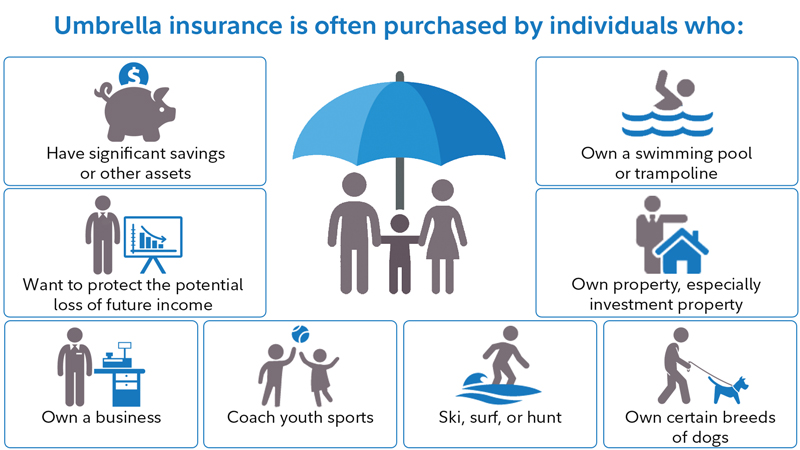

Do you need umbrella insurance?

Key takeaways Umbrella liability coverage protects against the potential financial fallout of certain types of unforeseen events that lead to property damage or injury, for which the policyholder is held responsible. An umbrella liability policy ...How Much Umbrella Coverage do I need?

How much coverage do you need? In assessing the level of coverage that may be appropriate, the following factors should be considered: The total value of all assets to be protected. All other things equal, the higher the asset value, the higher the ...Insurers to lawmakers: Health insurance policies 'were not designed' for pandemics

A group of associations that represent members of the insurance industry penned a letter to a pair of congressional lawmakers from California noting that its companies are not built to withstand pandemics such as the current coronavirus outbreak. ...Coronavirus to Spur Largest Single Loss in Insurance History – Chubb CEO

The, will likely spur the largest single loss in insurance industry history, said Evan Greenberg, chief executive officer of Chubb Ltd, during a call with analysts on Wednesday. Chubb, one of the world’s largest insurers, reported its first-quarter ...List of Auto Insurance Companies Offering Premium Relief

Which car insurance companies are offering relief? 21st Century: 25% discount on premiums in April AAA: 20% refund between for policyholders with insurance in effect from March 16 to May 15 Allstate: 15% discount on premiums in April and May ...